Article written by Aleks Vickovich and Lucy Dean. Published in The Australian Financial Review January 13, 2023.

Investors are preparing to plough money into shares and bonds this year even though market experts say the global economy is headed for a recession and the so-called 60/40portfolio – mixing growth and defensive assets – is dead.

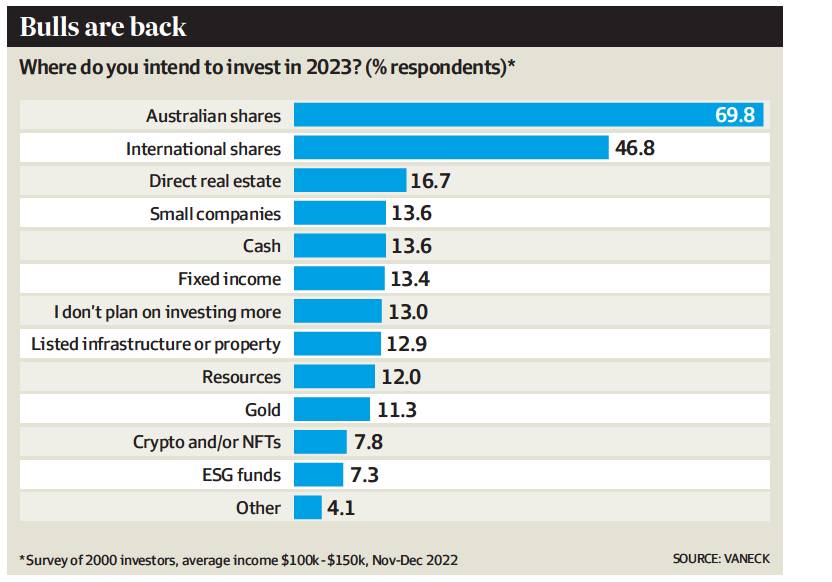

A survey of 2000 Australian investors by fund manager VanEck in November and December last year found most respondents (87 per cent) intended to kick-start or increase their investment in a range of asset classes, especially shares/ equities and bonds/fixed income.

The finding suggests the 60/40 strategy, which has historically underpinned the approach of many self-managed superannuation funds, might be experiencing a resurgence.

It was variously described by commentators as ‘‘dead’’, ‘‘broken’’ and ‘‘endangered’’ over the past year, as rising inflation hit the value of shares and bonds at the same time, in a rare occurrence.

The VanEck study found investors were most enthusiastic about Australian shares, with 69.8per cent of respondents planning to deploy capital to the local market, followed by international shares (46.7 per cent). Fixed income was selected by 13.4 per cent of respondents, receiving a warmer response than listed infrastructure and property (12.9 percent), resources/commodities (12 per cent), gold (11.25 per cent) or crypto assets (7.8 percent).

VanEck’s Asia-Pacific managing director, Arian Neiron, said the reasons the 60/40 approach ‘‘came into question over a year ago’’ had largely been erased, as the outlook for bond markets improved. Mr Neiron said he expected bonds to start playing a defensive role in portfolios once again, firming up the 60/40 thesis.

Martin Randall, head of alternatives at private wealth firm LGT Crestone, which advises some of Australia’s richest families, said the 60/40 strategy makes ‘‘far more sense today than it did 12 months ago’’, with interest rate rises dramatically altering the outlook for fixed income investments. ‘‘You can actually see value in bonds,’’ Mr Randall said. ‘‘You’re actually getting paid to own bonds, you’re getting paid in term deposits and fixed income instruments.’’

But while 60/40 might be slightly more attractive on the current outlook, Mr Randall said it was ‘‘too simplistic’’ to limit a contemporary, well-diversified portfolio to just two asset classes. ‘‘What worked in 1980 when the first concept of 60/40 came about doesn’t necessarily work today.’’

LGT Crestone has adopted a broad 50:30:20 philosophy made up of shares, bonds and alternatives (in that order) such as unlisted ‘‘real assets’’ (property and infrastructure),private equity investments and allocations to hedge funds. Its current ratio in a balanced client portfolio is 42 per cent shares, 35 per cent fixed income, 20 per cent alternatives and 3per cent cash.

Victor Smorgon Group, a high-profile family office, is even more bullish on alternatives, with an allocation upwards of 25 per cent. The group’s chief executive, Peter Edwards, said 60/40 might work for some conventional investment firms that want to ensure they’re ‘‘staying with the pack’’ and in a ‘‘comfortable position’’.

But since most of its portfolio is funded by the private contributions of members of Melbourne’s wealthy Smorgon family, the group is less constrained than some investors and able to take levels of risk that its backers are comfortable with.

‘‘Our view quite simply is, we can find better investments that pay us a higher rate, than whatever the interest rate is at the time,’’ said Mr Edwards, grandson of the former factory owner honoured in the group’s trading name. The group’s portfolio has no current exposure to bonds, for example, rendering the 60/40 prism irrelevant.

Financial adviser Travis Schindler, a partner at Hewison Private Wealth, agreed that investors should consider unique asset classes beyond stocks and bonds, describing the 60/40 approach as ‘‘outdated’’. He has advised some clients to invest in ‘‘secured first mortgages’’, for example, which share characteristics with alternatives and fixed income.

But he said investors were right to be more optimistic about the year ahead.

‘‘It’s hard to know what the 12 months ahead will look like,’’ he said. ‘‘What’s an easier question to answer is ‘what will turn the market around?’ and that’s likely inflation. There’s data to show that that’s coming down – that’s where markets will become a bit more confident and some optimism will show.’’

Fellow adviser Kevin Cardozo of Phase3 Wealth agreed that a 60/40 approach took an ‘‘arbitrary’’ approach to risk profiling and asset allocation. However, he said it still ‘‘made sense’’ as a way to think about diversification across risky and defensive assets.