After a prolonged period of low interest rates investors may have had good reason to direct surplus cashflow into investing, rather than knocking down the home loan. However, the equation is now much different.

With a rate rise announcement expected this coming Melbourne Cup Day, it further evokes the long-standing question – “do I pay off the mortgage, or invest my surplus cashflow?”

My objective in this blog is simply to provide you with the correct assumptions and considerations to make the right decision.

Many people would be mistaken to think the equation simply relates to the home interest rate, versus the investment return, specifically, the income/dividend of the investment.

So, let’s assume your mortgage interest rate is 5%, and the income/dividend return is 7%. You’d be best to direct surplus cashflow to the investment, correct? Not quite. Here is why.

Tax:

Each dollar of surplus cashflow earned has already had tax deducted from it, in other words, it is your after tax income. Therefore, to end up with $100 in your bank account you must understand the true cost of earning that $100 and add back the tax component.

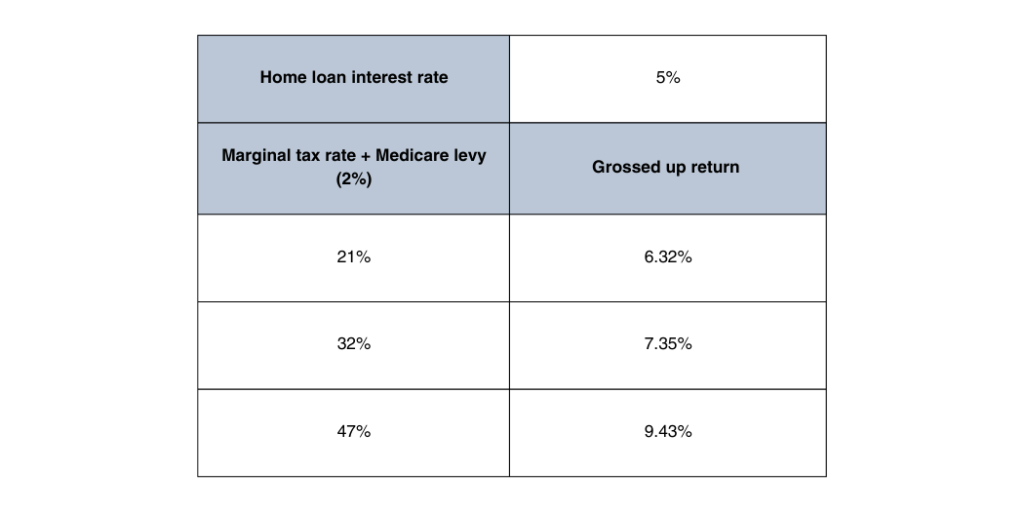

The equation required to calculate this is: home loan interest rate / (1 – income tax rate).

See table below:

The table above demonstrates that on a 32% tax rate, it becomes more beneficial to repay your mortgage, than invest elsewhere.

Investment returns:

It’s very important to remember that by repaying your mortgage, every dollar that you repay is akin to receiving a guaranteed return on the repayment, because that is exactly what it is.

For every dollar you repay from your mortgage, it results in a guaranteed return of the grossed-up percentage in the table above. Unfortunately, your financial adviser cannot guarantee your investment returns.

With this in mind, repaying your mortgage even when interest rates are low can make a lot of sense, given the guaranteed investment return nature of the repayment.

Arguably, there is no right or wrong answer and depends on the actual return of the investment alternative. Unfortunately, without a crystal ball there is no way to be 100% sure of its performance.

In the current environment of higher interest rates it seems that repaying as much of your mortgage as possible make most sense.

If you are very keen to invest and repay your mortgage in conjunction, you may consider using the equity in your home to re-borrow for investment purposes. The interest on this style of borrowing becomes tax deductible as it’s for investment purposes, however; it comes with its own sets of risks and considerations and professional advice should be sort before embarking on such a strategy.