As we end a calendar year, we now look ahead to the end of the financial year, and this means revisiting annual minimum pension requirements.

For Australians who have reached their preservation age and possess a superannuation account, comprehending the annual minimum pension requirements is crucial.

Upon reaching their preservation age, individuals can opt to withdraw funds from their superannuation as a regular income stream, known as a pension. However, to safeguard the longevity of an individual’s superannuation account, the government has established rules regarding minimum pension payments.

The annual minimum pension requirements stipulate that a specific percentage of an individual’s account balance must be withdrawn and received as pension payments each year. This percentage varies based on the individual’s age, ensuring that the withdrawn amount increases with age, further supporting their financial needs in retirement. Additionally, the minimum pension requirements set a baseline for pension withdrawals, while allowing individuals to withdraw amounts beyond the minimum if additional income is needed.

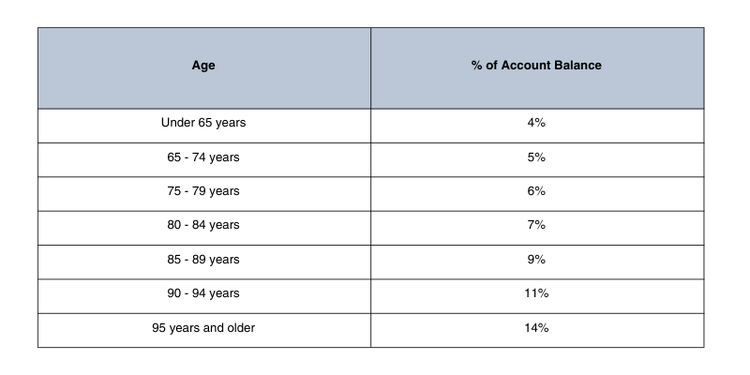

Calculations for the minimum pension requirements are based on the individual’s age and their superannuation account balance at the beginning of each financial year. The prescribed percentages for each age group are as follows:

Individuals heavily relying on these minimum pension payments must be aware of their obligations to avoid financial penalties. Failing to withdraw the required minimum can lead to taxation consequences or a loss of certain entitlements, such as the Age Pension.

It’s noteworthy that during the economic tremors of the COVID-19 pandemic, the nation’s pension and superannuation systems underwent a slight recalibration. This financial year marks a deliberate shift back to the pre-pandemic normalcy of minimum pension and superannuation percentages.

The economic upheaval prompted swift and necessary changes to minimum pension and superannuation percentages. Due to COVID-19, the Australian Government introduced a temporary 50% reduction in minimum pension payments for the 2019-20, 2020-21, 2021-22, and 2022-23 financial years. These measures were in response to the financial impacts of the pandemic, preventing retirees from being compelled to sell superannuation assets during market volatility. With financial markets stabilised, the pandemic concluded, and interest rates increased, the 50% halving has been removed.

For those in the pension phase, planning finances accordingly and being aware of mandatory pension payments is crucial, especially considering the return to the normal minimum percentages.

Seeking professional financial advice can assist in navigating the specifics of superannuation and ensuring compliance with annual minimum pension requirements.

By understanding and fulfilling these requirements appropriately, retirees can maintain a sustainable income stream while optimising their accumulated superannuation savings.